Dr. Pedro Gerber Machado works as a Researcher at Imperial Colleges’s Sustainable Gas Institute. Pedro is from Brazil and is interested in the sustainable development of energy production, thorough the development of new technologies and the application of policies. In this blog, Pedro talks about the inaction towards renewable energy in the last 30 years and how we need to change the history in order to have a true energy transition.

The definition of “transition” is not the most controversial definitions of all time, probably not even in the group of the 10 most controversial definitions found in the English language, if not in any language. Even so, the concept of “energy transition” seem to be of great controversy and a theme of great debate more and more as we reach the tipping point of climate change, that point in time which changes will be too late to be made. Taking the Cambridge dictionary definition, “transition” means “a change from one form or type to another, or the process by which this happens”.

Energy transition, nonetheless, has several definitions in academic papers, for example:

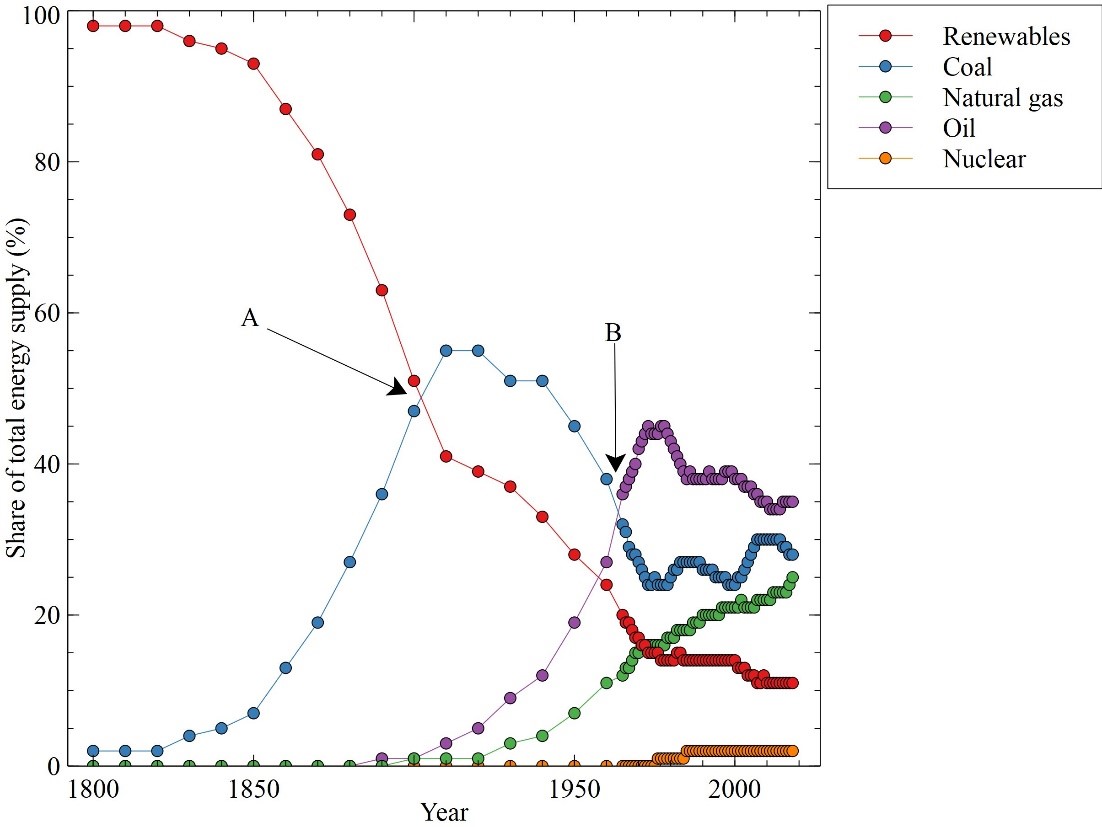

Figure 1 – global share of energy supply from 1800-2017 (%).

The arrows show the moment where the so called “energy transition” happened in the world. In a simple way, the transition is said to have occurred from biomass to coal in in the late nineteenth century and from coal to oil in mid-twentieth century. It seems like a true “transition”, in which biomass reduces, coal increases and later on coal reduces and oil increases.

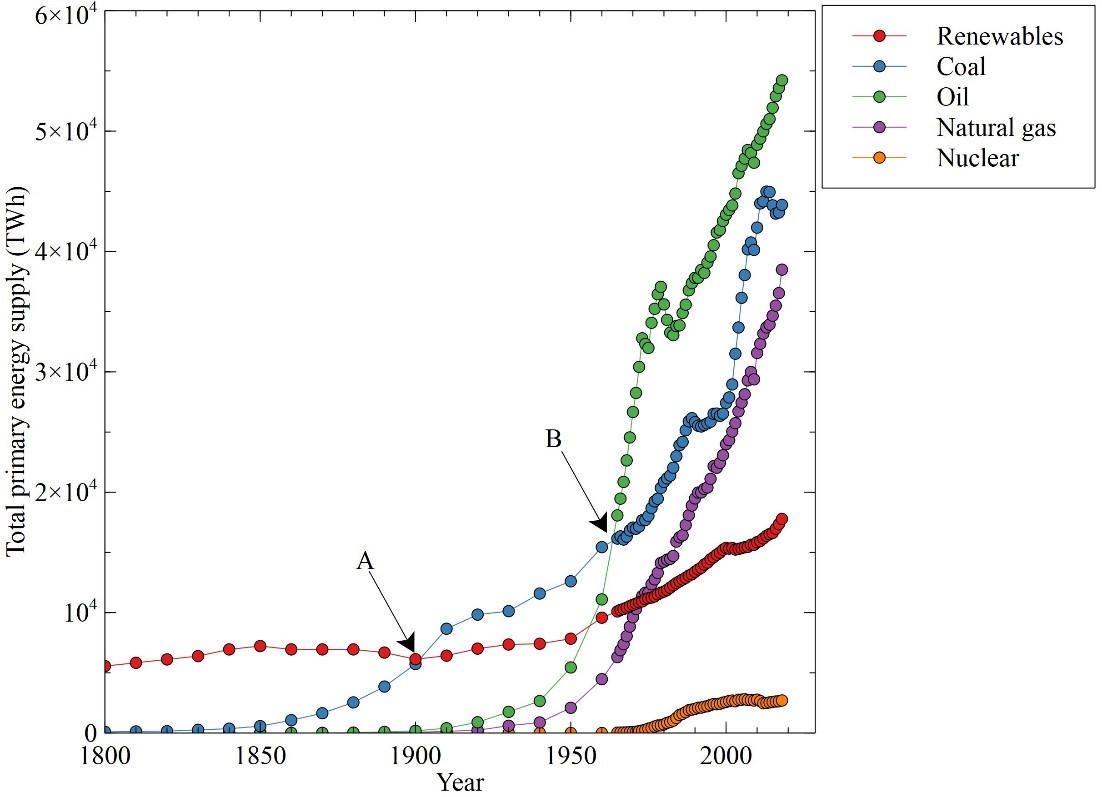

Let’s now take a look at the absolute primary energy supply in the line graph, with arrows showing the same moments in time when the “energy transition” took place.

When it comes to total primary energy supply, there was no “transition” (based on the dictionary definition), but instead what happened was a mere “addition”. In both moments there was no “change from one form or type to another”, simply because the other sources are still around. Traditional biomass was still around long after coal entered the energy matrix (and still exists today) and the same goes for the point when oil was introduced, there was no transition there, only an addition, since coal is still rising alongside oil, not falling.

Figure 2 – Total energy supply from 1800-2017 (TWh

Future transitions

More important than determining if what the world has gone through in the past was a “transition” or an “addition” is what is coming in the future and by the future we mean what is happening now. Transitioning away from our current global energy system is of paramount importance, since its negative environmental and social impacts are of global proportions and we are fast reaching a point of no return.

But it is also important to identify both the similarities and the differences between past and prospective transitions. A crucial issue is that, during past energy additions, both consumers and producers benefited from the new energy source. This is mainly due to lower fuel prices and the new developments in mechanics taking place during that those times. Whereas these private economic and financial benefits are not as obvious for low carbon energy sources and technologies, due to higher prices, generally. Moreover, the introduction of clean, low carbon energy sources has to take place in a real “transition”, and not repeat the same additions the planet has seen in the past.

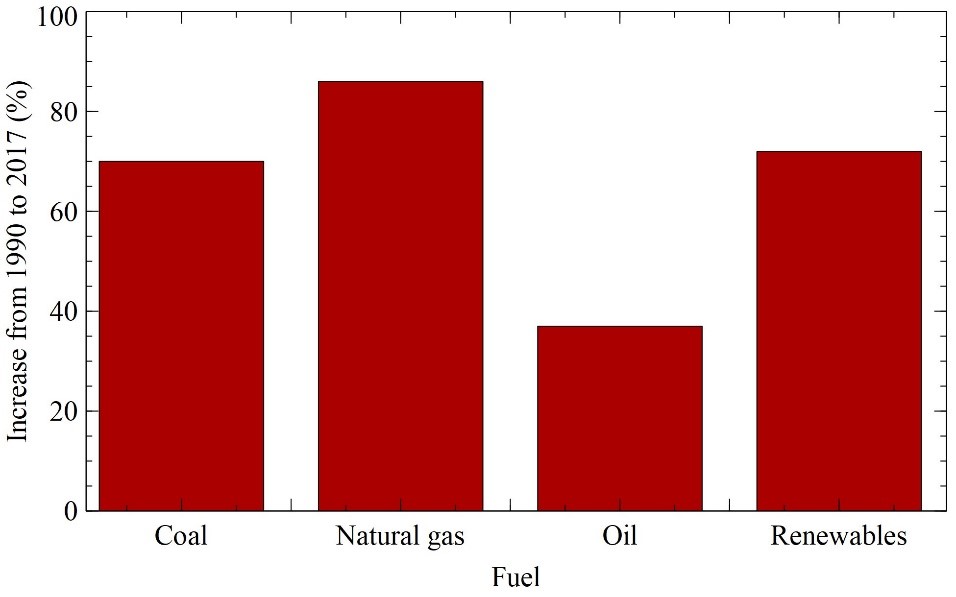

The bar chart (Figure 3) shows the relative increase of each energy source from 1990 until 2017. This is an important period due to the global increase in environmental concern over these past (almost) 30 years. There was Rio, there was Kyoto, there was Paris and still fossil fuels increased in production.

Figure 3 – Increase of each fuel supply from 1990 to 2017 (%).

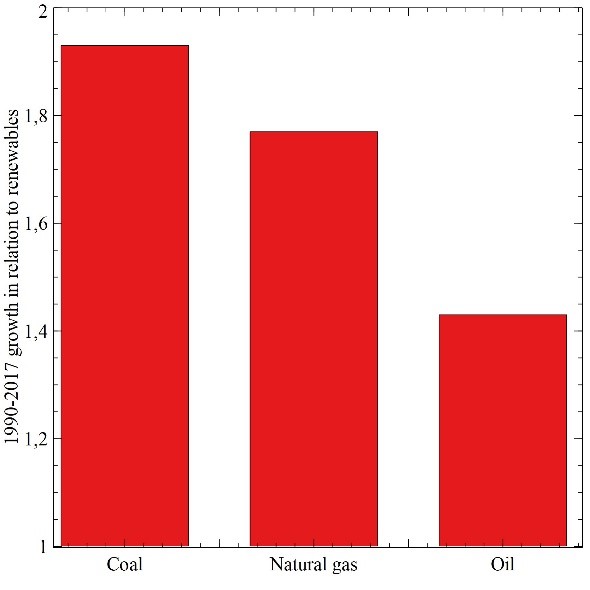

The problem, however, is worse when we see that the increase of fossil fuel has been, in absolute terms, higher than renewables in Figure 4.

Figure 4 – Increase of fossil fuels in relation to renewables from 1990-2017

What we see is that, for every 1 unit increase of energy from renewables in the last (almost) 30 years, coal increased 1.93, natural gas 1.77 and oil 1.49. In a world that needs to fully transition to renewables, this is not a good picture.

Unfortunately, this is a repetition of the past. Renewables are just being “added” to the energy matrix, while there is no reduction from the fossil side. This is incompatible with the desired climate change mitigation actions. To have a genuine transition, renewables need to increase in a proportion such that fossil fuels decrease in supply. Only then will the energy transition be an authentic out-of-the-dictionary transition, and not a trifling addition.

In this blog, PhD researcher at Imperial College’s Sustainable Gas Institute (SGI) – Diego Moya reflects on the recent SGI Annual Lecture: Practical Action for a lower carbon footprint by CEO of Oil and Gas Climate Initiative Climate Investments, Dr Pratima Rangarajan.

On the 30 October 2019, the SGI hosted Dr. Pratima Rangarajan, the first Chief Executive Officer of the newly formed climate investments company: The Oil and Gas Climate Initiative (OGCI). The 13 OGCI member companies represent 32% of the global oil and gas production and have invested US$ 6.5 billion altogether in low carbon technologies by 2019. OGCI Climate Investments aims to accelerate the development and deployment of innovative technologies that have the potential to significantly reduce greenhouse gas emissions on a significant scale across the globe.

Drawing upon her rich experience on the energy arena, Dr. Rangarajan has been the General Manager of GE’s Onshore Wind Product Line and GE’s Energy Storage as well as the Deputy Chief Technology Officer and Senior Vice President at Vestas Wind Systems.

Medium-term investments for long-term impacts

Source: OGCI presentation, IEA WEO 2018

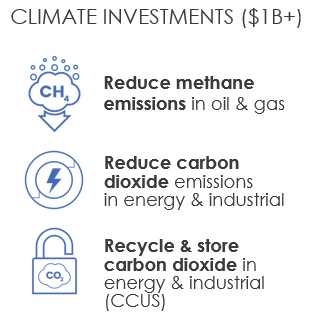

As three quarters of the total greenhouse gases come from the power and industry sectors, the OGCI initiative has set a target to invest US$ 1 billion-plus in those sectors over the next decade, focusing on long-term impact. With this investment, OGCI members expect to seriously reduce their collective methane emissions by approximately 0.6 million tonnes. This is greater than a third of the methane produced annually by the end of 2025.

OGCI Climate Investments has identified three main aims of their capital investment practices: (1) Reducing methane emissions; (2) Reducing carbon dioxide, CO2, emissions; and (3) developing carbon capture, utilisation and storage (CCUS), which they also called “Recycle & store carbon dioxide”. Let’s elaborate on these aims:

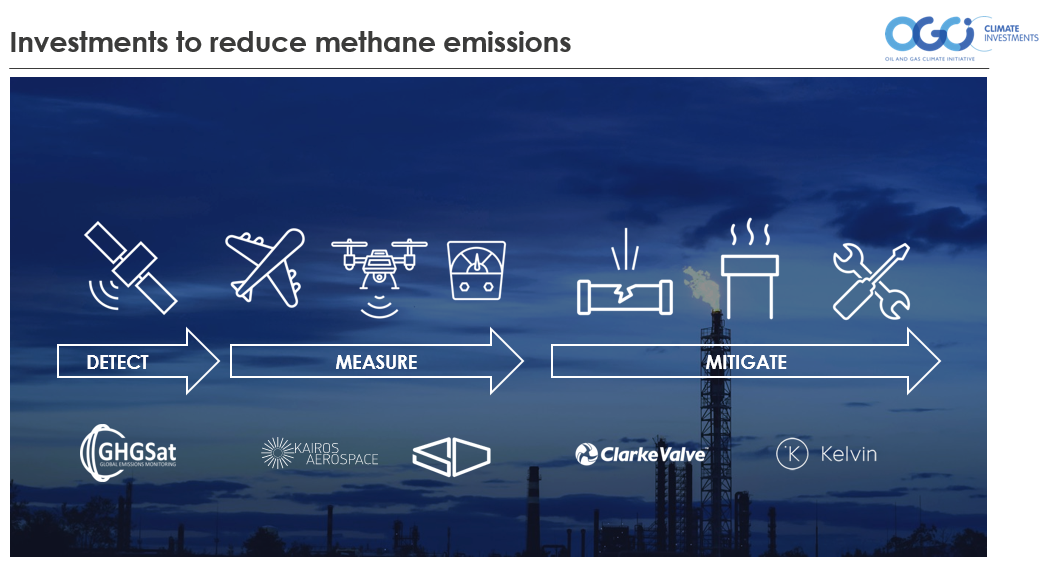

1. Reducing methane emissions

Source: Slide from OGCI presentation

After carbon dioxide (CO2), methane emissions are the second most abundant anthropogenic GHG present in oil & natural gas systems, combustion, and certain industrial processes. Methane is more than 25 times as potent as CO2 at trapping heat in the atmosphere and accounts for approximately 20% of global emissions. Thus, significant GHG reductions can be achieved by a rapid and effective drop of manmade methane in the atmosphere.

OGCI plans to reduce methane emissions by investing in five technologies in three specific stages (detection, measurement and mitigation) of methane mitigation. At the detection stage, a global satellite-based remote sensing technology, GHGSat, provides greenhouse gas monitoring services to accurately detect facility-level emissions. Then, Kairos Aerospace and a drone-based technology SeekOps measure methane emissions. In the mitigation stage, both ClarKe Valve and Kelvin technologies have collectively reduced methane intensity of OGCI members by 9% in 2018. These technologies in all stages finally contribute in improving productivity while reducing emissions.

Source: Screenshot of GHGSat website

2. Reducing CO2 emissions

CO2 emissions account for about 70% of global anthropogenic GHG emissions. In contrast with the short-lived of methane, CO2 can remain in the atmosphere from a few years to thousands of years. The second focus of OGCI Climate Investments is reducing CO2 emissions through increasing energy efficiency in the industry, transport and buildings sectors. Since almost two-thirds of primary energy is lost from production to end-use, OGCI’s actions are focused on improving energy efficiency and reducing wasted energy. In the industry sector, OGCI invests in the Boston Metal technology which cost-competitively produce emissions-free steel.

Three technologies (Achates, XL, Norsepower) have also received OGCI investment to provide high fuel-efficiency opposed-piston engines, plug-in hybrid heavy-duty commercial vehicles, and mechanical rotor sails for ships, respectively. In the buildings sector, the 75F technology enables energy savings from heating, cooling and lighting, providing a joint hardware and software product to manage energy consumption in commercial buildings. These energy efficiency technologies target the 40% of the abatement required by 2040 to meet the Paris Agreement goals.

3. Recycle & store carbon dioxide

CCUS is being mainly applied in industry and power sectors, involving (1) the capture of CO2 from fuel combustion and industrial processes, (2) the transport of CO2, and (3) its use to create other products or services, or its storage in geological formations. To accelerate the CCUS industry, OGCI Climate Investments is developing 5 CCUS hubs via private and public partnerships worldwide.

This aims to create the necessary market conditions (policies) for substantial investments by OGCI member companies to decarbonise industry hubs around the globe. OGCI Climate Investments has made investments in five technologies for recycling and storing CO2, ranging from CCUS in enhanced oil recovery fields to CO2-based concrete cured and CO2-based polyurethane products.

Are massive capital investments in low carbon technologies enough to reduce greenhouse gas emissions?

In my opinion, clearly, not. Unfortunately, capital practices, technology development and the natural conditions of the planet for sustainable production are clearly incompatible. If we want to limit the temperature increase to less than 2 degrees by 2100, we must dramatically reduce human-activity-based emissions, starting right now in industrialised countries. However, it is difficult for global companies to fully accept this proposal because it is incompatible with their businesses. Massive investments in low-carbon technologies would be certainly not enough. We also need to “invest” in a change toward an ecological civilization.

We have not yet decoupled economic growth (GDP) from carbon emissions. The challenge is for developing economies that may suffer from runaway emissions in a close future. We can see that the technological development is triggered/driven by capital forces of global companies which also leads to the full development of the negative aspects of technologies in the fact that capital can take advantage of even the ecological disaster that the same capital-intensive companies have greatly created. Inventing new business opportunities to benefit the capital from the current economic and environmental crisis would clearly exceeds the natural limits of the planet and is indeed a contradiction with the current level of human civilization. Decoupling GDP from carbon emissions will certainly require a set of environmental policies and a move to less carbon-intensive economy sectors.

A serious commitment to global warming simultaneously requires a conscious struggle against the way we use and consume energy and materials. Energy AND material flows should be jointly assessed which will require to explore the energy consumption and consumerism toward the production of unnecessary goods. Recent scientific progress has identified that a critical analysis of combined economic policy and natural sciences is needed for a radical change in the increased of energy demand and materials consumption across whole economy sectors.

We truly need to re-establish production systems that strike a balance between human beings’ progress making sure we use our natural resources sustainably. This radical change should not only consider massive capital investments in low-carbon technologies but also leaving fossil fuels in the ground, exponentially increase the deployment of renewables and most importantly changing the growth paradigm, where the planet’s resources and the natural environment must be handled with care.

Diego Moya works as a PhD researcher at Imperial College’s Sustainable Gas Institute, and is also part of the Science and Solutions for a Changing Planet DTP at the Grantham Institute – Climate Change and the Environment. Diego from Ecuador is interested in the sustainable development of the Latin American region and is one of the founders of iiasur (Institute for Applied Sustainability Research). In this blog, Diego explores how the region could move towards a low-carbon economy.

Latin America and the Caribbean (LAC) covers an area equivalent to the combined surface area of the USA and China. Despite its vast number of agricultural products and natural resources, and the fact that it has the largest reserves of petroleum (in Venezuela), natural gas, and freshwater, Latin America still has a number of challenges to overcome to achieve widespread welfare and development.

Hydropower plant. Curtesy of Dan Meyers. Source: Unspla

Climate change is also increasing extreme weather events in the LAC region. In 2017, Peruvian president declared a state of emergency after Lima’s worst floods killed 67 people and damaged 115,000 homes. This year in Mexico, wildfires tore through drought areas burning nearly 150,000 hectares. Intense rains, uncontrolled forest fires, agricultural productions losses and long droughts due to intense weather conditions are risking the lives of 660 million LAC citizens.

Having insufficient infrastructure, limited resources and a critical knowledge gap also make the region unable to adapt to such catastrophic climate change impacts. However, past and current emissions produced from industrialised economies are truly the cause of climate change worldwide. Those nations and people who have made the least contribution to climate change are bearing the burden while lacking the wealth to cope with its effects.

What are the low-carbon options to tackle climate change in the region?

Installed Capacity of non-renewable energy. Source: OLADE

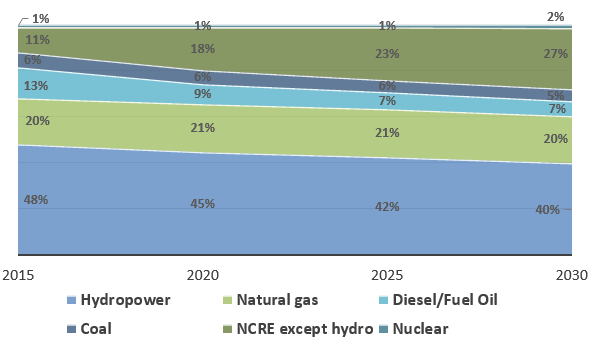

Despite having an unfavourable climate change adaptation situation, LAC economies are well positioned to move towards the zero carbon-energy target. According to OLADE (the Latin American Energy Organization), large hydropower remains the biggest renewable power source in the region with a share of 45 % in the total power installed capacity mix. However, extreme weather patterns and the growth of other renewables is changing the mix. Although hydropower will remain strong, other renewables could increase considerably.

Fortunately, there are also opportunities for other cleaner technologies to meet the minimum level of demand on an electrical grids (baseload power demand); the technologies could be geothermal and natural-gas power plants (as a cleaner option to switch from other fossil fuels). While geothermal-based technologies can meet long-term emission targets, geothermal resources are location specific and therefore distribution costs can be unattractive for investors. Expanding natural-gas-fired power would help meet short-term emissions targets when switching from other fossil fuels but would also encourage the long-term reliance and use of it.

So what is the emission reduction potential in LAC’s economic sectors?

Agriculture – enhancing reforestation

Harvesting. Source: Photo by Urip Dunker, Unsplash.com

Although the agriculture sector in the LAC region is not highly industrialised yet (energy consumption is minimum compared with the other sectors), the loss of forest for agricultural land is releasing carbon emissions at shocking rates. Greenhouse gas emissions related to agriculture are linked to livestock, rice production, agricultural soils management and biomass burning.

Forest regulate ecosystems and play an essential part in the carbon cycle. LAC countries contain 22% of the world’s forest area. However, deforestation for agricultural land is a major issue currently facing the region. The rate of deforestation in the region is alarming; between August 2017 and July 2018, an area of Amazon rainforest, equivalent to five times the size of London, was destroyed in Brazil.

Loss of forest also contributes approximately 10% to annual global greenhouse emissions. Therefore, countries that share the Amazon rainforest (e.g. Brazil, Venezuela, Colombia, Ecuador, Peru, Bolivia) need to implement strong mechanisms to control land-use and enhance reforestation in the Amazon to achieve carbon mitigation targets.

In 2019, INPE (the Brazilian The National Institute for Space Research) has detected 72,843 fires across the Amazon basin.

The food and agriculture organization of the United Nations (FAO) promotes Sustainable forest management across the region. However, just a few countries have joined the initiative (Argentina, Chile, Costa Rica and Dominican Republic). The program aims to put in practice relevant models of sustainable land use and conservation of forest resources. They work together with local partners to strengthen model forest development in the region.

Finally, policy makers also need to take into account the additional required to modernise the agricultural sector in LAC countries in their energy planning. The use of modern methods would give greater productive yields (e.g. mechanised equipment to plough a field). Although additional energy is needed to power pumps, for irrigation or switch from kerosene lamps to electricity light, this would not only improve agricultural productivity but also, most importantly, it would improve the life quality of people working in the rural sector and farms.

Transport – investing in low-carbon infrastructure

The LAC region lacks a low-carbon transport system. The largest share of energy demand is the transport sector (37%) and the growing rates of car ownership create a market opportunity to both electrifying the sector and expanding cleaner fuels (i.e. bio-fuels, natural gas). The average car ownership rate in LAC countries is 6% annually compared with about 1% in industrialised nations such as the UK, Germany or the USA. More investment is required in public transport systems across the region. Railways, light rail systems and subways to interconnect big cities and countries were not considered in the development of the region.

Transport via tram. Source: Pixabay

But there is still a huge opportunity for foreign investment, capacity building and tackling poverty in the region by developing a sustainable transport system. There are some good examples across the region. In Argentina, the 2008 railway reorganization act resulted in major projects such as the Circunvalar Ferroviario light rail system in Rosario along with electric underground lines in the metropolitan Buenos Aires area and upgrading sections of the Belgrano-Cargas railway. In Chile, use of electric-buses is growing fast; Santiago aims to have 80% of its public fleet driven by E-buses in 2022.

Industry – improving efficiency

The industry sector is responsible for 31% of the total energy consumed in the LAC region. The demand for heat and electricity in industrial processes such as beverages, tobacco, metallurgy, textiles, footwear, cement, steel, and textile has made the region an important focus for clean technologies deployment (i.e. Brazil, Argentina, Chile and Mexico). Electricity penetration and fuel substitution are key for industrial expansion in the region. Process that require to produce heat or cooling are ideal to increase industrial electricity use and reduce fuel consumption.

LAC’s energy intensity – the ratio between energy consumption and GDP of a country – has remained almost constant in last decades. This is mostly due to weak energy efficiency policies and its implementation. The most high-intensity industries in the region are mining, chemicals, pulp and paper, iron and steel, and cement sector. These industrial sub-sectors should promote the use of (1) energy management systems and energy efficiency projects, (2) the best available high-efficiency industrial equipment and capacity training, and (3) energy efficiency products and services from small and medium enterprises (i.e. energy audits).

Residential – the most electrified end-use sector

The residential sector accounts for about 16% of the end-use energy consumption in the region. The region has moved from traditional solid biofuels to more efficient appliances, heating and cooling technologies. However, the consumption of electricity and natural gas is still inefficient due to lack of insulation in buildings, inefficient cooling technologies, inefficient lighting and poor water heating technologies. Although the LAC region is close to achieving universal energy access, still 15 million people live without electricity and over 56 million people rely on traditional uses of solid biofuels for cooking and heating.

Energy efficiency in buildings is also still an issue. Improving building fabric, upgrading insulation, switching to more efficient technology (i.e. electric stoves, district gas networks) and using SMART systems are key to improving life style while keeping low energy consumption in the region.

COP25 Chile 2019: a huge opportunity to discuss the low-carbon future of the LAC region

Now that it is Latin America’s turn to host the next COP25 in Chile later on in November 2019, we can see a huge opportunity to discuss the geopolitical implications of a more sustainable development of the LAC region. COP25 in Chile will highlight a number of current global issues.

The discussion around these topics at the COP25 in Chile is the opportunity to start the debate around the root of the unsustainable development of the LAC region. In my opinion, both the extraction of raw materials without the industrialization of end-use products and the lack of local capacity building, has produced a critical knowledge gap and a lack of technology innovation that has affected the development of our economies.

My final thoughts are that…

Multinational corporations along with governments must commit to developing local capacity to transform cheap raw materials (extracted in the region) into profitable manufactured goods. This would require a set of policy instruments to develop a long-term roadmap to fill the knowledge and technology innovation gaps that would eventually enhance the low-carbon development of our region.

Governments, foreign industry working locally and academia in the LAC region need to work together. We definitely need to explore competitive advantages through innovation by solving local problems at all scales of development in a sustainable way. The implementation of new science and innovation policies and strategies must reflect a sustainable development of the region otherwise we will progress at the expense of the environment.

Acknowledgement

I acknowledge the valuable comments and suggestions made by Dr. Pablo Carvajal.

About the author

Diego works as PhD researcher in the MUSE energy system model Group at Imperial College’s Sustainable Gas Institute and is part of the Science and Solutions for a Changing Planet DTP at the Grantham Institute. Diego is supported by SENESCYT Universities of Excellence Scholarship Scheme and Universidad Técnica de Ambato (UTA). He is a scholar of the Faculty of Civil and Mechanical Engineering, Technical University of Ambato, UTA-Ecuador. Diego is also one of the founders of iiasur (Institute for Applied Sustainability Research) [LinkedIn, Twitter].

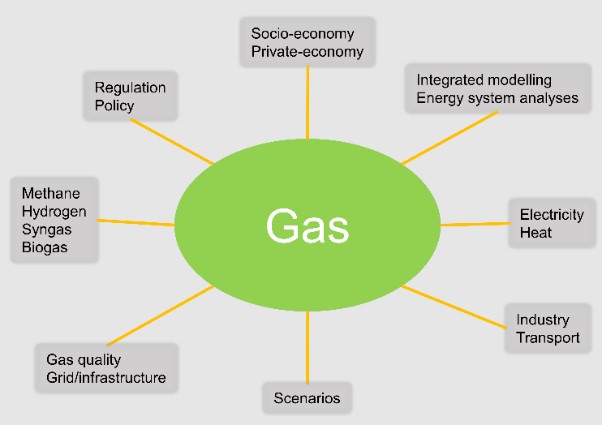

This article was written by a Ph.D. student Rasmus Bramstoft from the Technical University of Denmark who is currently on a placement at the Sustainable Gas Institute with the MUSE team. For his PhD , Rasmus is exploring the role of gas in future renewable-based energy systems in Denmark as part of the FutureGas project using a combination of global and regional energy systems models.

Energy Crossroads

We are currently at an energy crossroad; climate change is happening now and will continue rapidly if we do not act. Globally, nations are joining forces to take action, and the Paris Agreement aims to limit the raise of the global temperature to well below 2⁰C or even 1.5⁰C compared to the pre-industrial temperature. The energy system is currently a major contributor to global greenhouse gas (GHG) emissions. Countries have therefore set their own national energy and climate targets and visions. The Nordic countries, including Denmark, are a pioneer in implementing renewable energy sources (RES).

Role of gas in Denmark in 2018

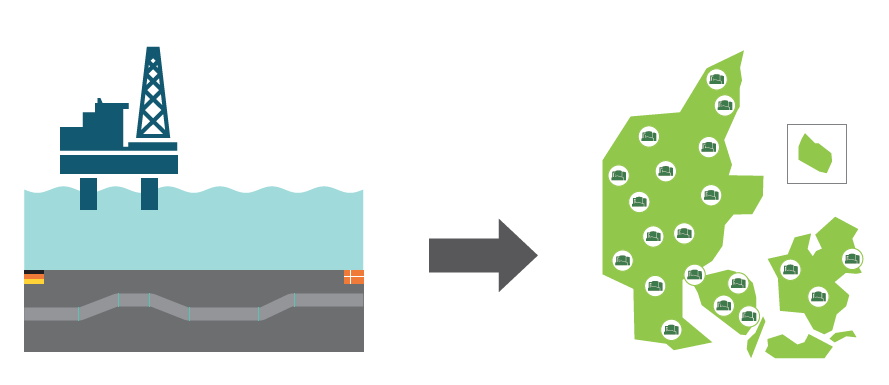

In Denmark, gas accounts for 16% of the national energy consumption. Denmark has large, but limited reserves, of natural gas in the North Sea. However, national gas production is undergoing a transition from centralised fossil fuel based production to decentralised energy production based on renewable energy sources. This transition is happening now, and a record was set last summer, where in July 2018, 18.6% biomethane was injected in the gas grid compared to the natural gas consumption in Denmark.

Exploring the role of gas in future energy systems

To investigate the role of gas in future energy systems, you really have to understand the complete energy chain from production, via transportation and storage, to the end-consumer. This is what we are doing with the FutureGas Project, which is a project evaluating the role of gas by combining various disciplines from technical aspects to policy barriers and energy systems modelling.

Energy system models provide insight into future energy trends

Energy system modelling is a discipline, which can provide valuable insights into future energy trends. Models are developed using different approaches (e.g. bottom-up vs. top-down, or optimisation vs simulation), assumptions (e.g. different scenarios) and covering different sectors (e.g. power, district heat, gas, and transport) with diverse geographical and temporal resolution. The purpose behind these differences is that each model can answer a specific research question.

How to model gas in future energy systems

The energy system is incredibly complex, and therefore models need to take into account these complexities. For example, gas can be used in various sectors (power, heating, industry, residential, and transport). Moreover, large energy quantities can be stored in underground gas storages. It is, therefore, crucial to investigate the role of gas in future energy systems using a holistic energy system assessment tool, such as the Balmorel-OptiFlow model, in order to understand all energy sectors (power, heat, gas and transport fuels) and their relationship with each other.

Electricity is a key energy vector that also has to be considered, and is seen as the backbone system of the future. However, future generation from variable renewable energy sources (VRE), such as wind and solar, calls for system flexibility due to the intermittent nature of these sources, which can be provided by system integration with gas through, for example, through power to X (PtX) where power is converted (directly or in combination with other resources) into gas or fuels.

System integration also gives us another possibility, for example, technologies which produce by-products (e.g., excess heat) can be sold as heat to district heating networks and receive an additional flow of income. Examples include biorefineries, and combined heat and power plants.

Finally, the integration of cross-border infrastructures such as the power and gas transmissions systems allow energy to be balanced.

Best practice in energy systems modelling

When modelling future energy systems, it is important to consider the following features:

A holistic energy system perspective covering the complete energy system;

Take into account existing infrastructure and any decommissioning of existing plants;

Allow investment and operation optimisation to investigate the most cost-efficient transition pathways;

High geographical resolution; covering a large geographical area, and allowing for detailed resolution of energy resources;

High temporal resolution; to simulate the variable and fluctuating production from variable renewable energy sources (VRE) technologies such as solar and wind.

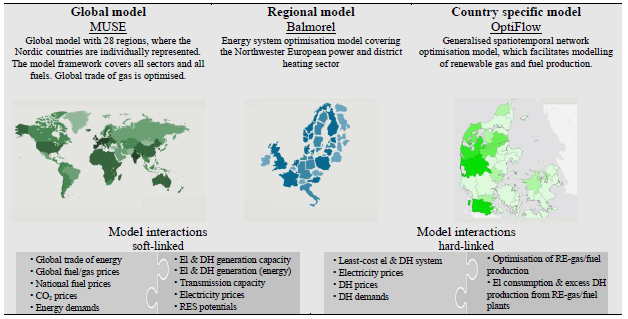

Combining models: MUSE and Balmorel

Gas is used all over the world.

Modelling the role of gas and renewable gas at different geographical scale, for example global, regional (Northern Europe), and country (Denmark) level, is a remarkable contribution to the research field and can be used to support stakeholders and policymakers in strategic decision-making to identify promising pathways and conversion technologies.

At the moment, I’m working on developing a modelling framework where we combine the MUSE energy system model, developed by the Sustainable Gas Institute, with Balmorel-OptiFlow modelling.

MUSE provides global whole system results, while Balmorel-OptiFlow provides results for the integrated electricity, gas and district heating systems, with higher temporal and spatial resolution for North-western Europe.

In this way, the novel modelling framework combine assessments of global prices of energy carriers with detailed modelling of the chain from the transportation of primary resources to renewable gas production plants, through storage facilities and to end consumers, while taking into account the spatial and temporal energy system integration. The co-simulation leads to the socio-economic optimal system, where investments and operations optimisation is facilitated for the integrated energy system.

Further reading

FutureGas – The integration of gas in the future Danish energy system. Published: “Gas for Energy” 03-2017, ISSN 2192-158X – Poul Erik Morthorst, Marie Münster, Tara Sabbagh Amirkhizi, Rasmus Bramstoft.

This article was written by Siyuan Chen, a Ph.D. student from Tsinghua University in China who is currently on a placement at the Sustainable Gas Institute. Siyuan in this article describes an energy model that his team is working on that aims to address the huge air pollution problem in China.

The haze weather in Beijing. (Source: http://news.takungpao.com)

Air pollution problem in China

Over the last few years, air pollution has become a severe problem in China, especially the haze problem. From 2013 to 2016, Beijing experienced haze weather for 183 days each year on average. The wide range of haze weather causes many problems including traffic jams, flight delays, and increasing respiratory disease. There are many reasons for the severe air pollution problem in China, which include vehicle exhausts, construction dust, factory fumes, and coal combustion. However, coal combustion is considered as the major contributor to air pollution, and in China, more than half of the coal consumption is for electricity generation.

Therefore, cleaner production in the power sector plays an important role in tackling the air pollution problem. So how can China ensure it reduces the environmental impact of power generation, and how can energy systems modelling help?

Coal power plant (Source: Pixabay)

Action plan for air pollution prevention and control

In order to solve this urgent air pollution problem, the Chinese government launched the “Action plan for air pollution prevention and control” in 2013. The action plan aims to reduce the inhalable particulate concentration by over 10% in 2017 compared with 2012 levels. At that time, ultra-low emission technologies of coal-fired power plants were developed and first deployed in 2014. Sulfur dioxide (SO2) and nitrogen oxides (NOx) emissions from coal-fired power plants equipped with these emission control devices are lower than 35 and 50 mg/m3 with 6% oxygen content respectively, which is as clean as gas-fired power plants. In order to address the air pollution problem, the Chinese government plan to retrofit all qualified coal power plants with ultra-low emission technologies by 2020.

However, the policies are still vague and the impacts of this change are unknown. So it is essential to find a cost-effective clean production pathway for China’s power sector to address the air pollution problem.

Power generation expansion planning considering environmental issues

Power generation expansion planning is used to determine the optimal type, location, and construction time of power generation technologies whilst ensuring that the increasing power demand is met. Recently, environmental issues have been taken into consideration due to the growing concern of global warming and air pollution.

To deal with China’s air pollution, it is important to conduct power generation expansion planning with environmental constraints. At Tsinghua University, we have developed a model, known as the Long-term Multi-regional, Load-dispatch and Grid-structure based power generation planning model (LoMLoG), to support the decision-making process to help planners understand the environmental issues.

The model takes into account the following four factors:

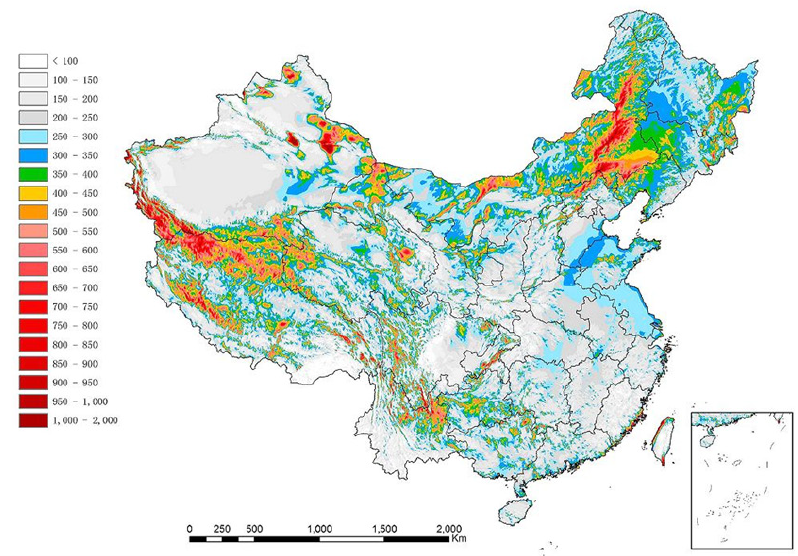

Wind resources are mainly located in western and northern China (Source: Sino-Danish RED Prog).

1. Uneven distribution

Natural resource and electricity demand in China have an uneven spatial distribution. China has abundant resources in western areas, such as fossil fuel and non-hydropower renewables in Xinjiang and Inner Mongolia and hydropower in Yunnan and Sichuan. However, power demand in eastern coastal areas (e.g. Shanghai, Jiangsu, Zhejiang, and Guangdong) is much greater than in these resource-rich regions. Based on these regional characteristics, China is divided into seventeen areas reflecting power demand and natural resources.

2. Power transmission

With the rapid development of long-distance Ultra-High-Voltage power transmission lines in recent years, eastern coastal areas of China are capable of importing electricity from western areas which have abundant natural resources, instead of constructing power generation facilities locally. Long-distance cross-region power transmission options could have a great influence on regional power generation structure and give new insights to policymakers for air quality control. Therefore, we have included power transmission among regions in this model.

3. A temporal module

Electricity demand has high volatility in a 24-hour period on a day-to-day basis, and also from season-to-season. It, therefore, needs an accurate and reliable electricity supply to match the needs. From the electricity supply side, renewable energy also has a high temporal variation and can be used only when resources are available, which increases the uncertainty of the power system. In order to handle this problem, a temporal module is introduced. We have therefore divided each year into four seasons and each day is divided into twenty-four hours to capture the high time resolution of the power system.

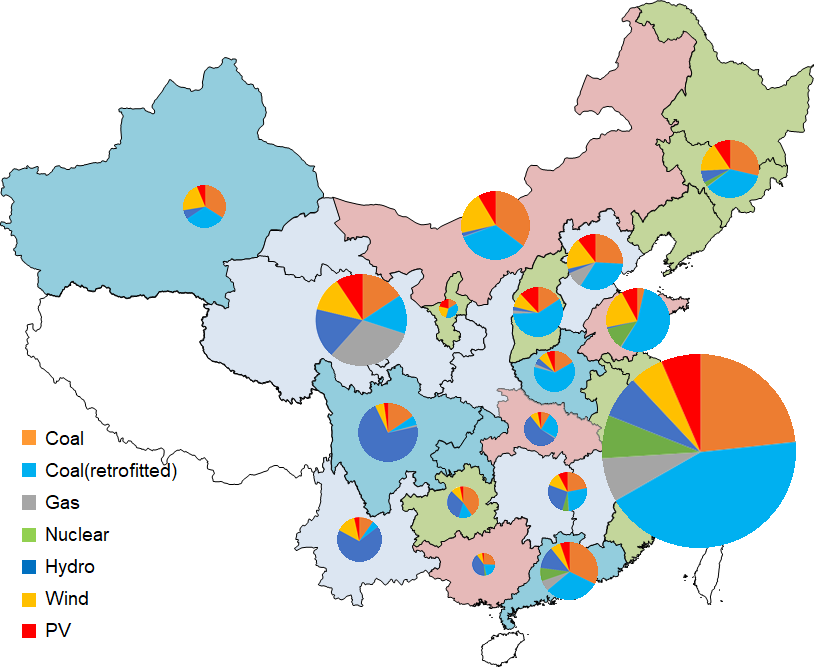

The capacity mix of power sector in all regions is shown.

4. Emissions targets

According to the 13th Five-year Plan for Eco-environmental Protection issued by the State Council, national sulfur dioxide (SO2) and nitrogen oxides (NOx) emissions must be reduced by 15% in 2020 compared to 2015 levels. The emission reduction targets set by the government are therefore also incorporated into the model as must-achieve goals so that air pollution can be controlled.

Cleaning up the power sector

Our model presents a cleaner way for the power sector to reduce and control air pollution. The results show that ultra-low emission coal power plants would account for 60.5% of total coal power plants by 2020. The capacity of renewable energy (wind, solar PV, hydropower) would account for 36% of total power generation units. Due to the large-scale deployment of ultra-low emission technologies in coal power plants and rapid growth of renewable energy, SO2, and NOx emissions would decrease by 44% and 21% in 2020 compared to 2016 levels.

The regional capacity expansion pathway of power sector is also shown in the results. Thanks to the construction of long-distance Ultra-High-Voltage power transmission lines across China, eastern coastal areas with greater air pollution could import a great deal of electricity from western and Northern China, which helps them to decrease local coal power generation and air pollutants emissions accordingly.

Future work

Air pollution control is generally the short-term goal of China’s energy system. In the long term, climate change issues will need more attention. China has made a firm commitment in the Paris Agreement and has become an important participant, contributor, and torchbearer in the global endeavor for environmental civilisation. Therefore, it is vital to find a low-carbon transition pathway for China’s power sector, which would be the focus of future work.

Sustainable Gas Institute (SGI) has developed a global whole system model (MUSE) to simulate energy transitions towards a low carbon world. The model has rich types of technology and novel modelling methods, which can be a good reference for China’s low-carbon energy transition. During my research stay in SGI, I would like to learn these advanced methodologies and conduct cooperative research work on China’s low-carbon energy transition pathway.

Chile is committing to decarbonising its electricity sector with a target of 60% renewable power by 2035, but there are still some challenges with decarbonising the heat sector. Chileans still rely heavily on natural gas to heat their homes. Jorge Salgado Contreras from Chile, visited the Sustainable Gas Institute for two months, funded by the Chilean National Commission for Science and Technology, and tasked with investigating ways of developing heat decarbonisation pathways for cities in Chile. We interviewed Jorge about his research.

What is your background?

I am an industrial engineer and now Head of the Electrical and Electronics Department at Inacap in Punta Arenas University, Chile. I have combined experience in the energy sector, working in academic, private and public sectors. In the private sector, I have worked for both the national gas retailer (Intergas Inc) on both business development and the technical side, as well as in an energy start-up. I also worked for the Ministry of Energy of Chile, on renewable energy and energy efficiency projects, where I was in charge of cogeneration initiatives and lead the long-term energy plans for two cities in Patagonia.

How did you find out about the Sustainable Gas Institute, and what first sparked your interest in working here?

I found the Sustainable Gas Institute website, and it was actually the name that first caught my attention. I really liked the aims of the Institute as it is clear we cannot move to 100% renewables straight away, and a transition is necessary. I also thought the White Paper Series is really trying to address some unresolved issues. Even though the reports are written by academics, they are very influential from a policy context.

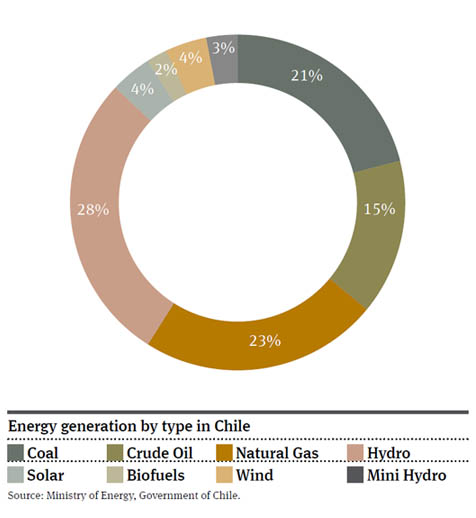

The energy mix in Chile (Source: Ministry of Energy, Chile).

Your project is to understand how to decarbonise heat for Chile. Can you tell us why it’s so important an issue?

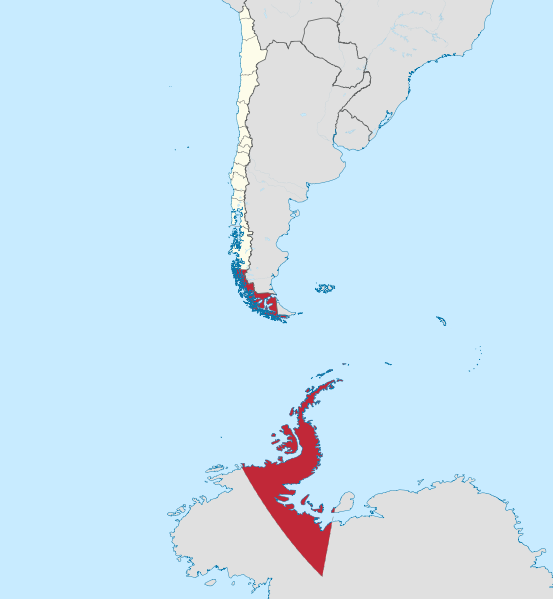

Chile is actually very cold, especially the southern end which is where I am from; it can go below -10 °C. While Chile has ambitious climate targets to increase renewables to 70% by 2050, these targets have only been set for the electricity sector and there are little targets, plans or research taking place to reduce the emissions intensity of the heat sector.

We currently use so many energy to heat our homes in Chile. Fortunately, Chile does have a good renewables portfolio (22% renewables), increasingly with solar and wind. However, in my region (Magallanes and chilean Antarctica, Chile), we still use natural gas to heat our homes, as you do in the UK. We do have access to our own natural gas and biomass but in other regions, for example in Southern Chile, natural gas is imported from overseas. The natural gas subsidy for residential and commercial use in the Magallanes region is around 100 million US$/year and represents about 70% of the Chilean Ministry of Energy National Budget.

What is the project about and who have you been working with?

I have been trying to understand whether we can work with low-carbon options such as hydrogen to decarbonise the existing gas grid infrastructure. In Chile, there is not much research taking place to understand the role of hydrogen in heat decarbonisation.

I have also been looking at the use of electrification and technologies, such as heat pumps. The recent report by the UK Committee on Climate Change into this was very useful as a case study. The idea is to adapt for the Chilean context, and we could move forward towards a low carbon economy by replacing natural gas with hydrogen.

At the Institute, I have been mainly working with both Dr. Paul Balcombe (an expert in the supply chain for hydrogen) and Dr. Francisca Jalil Vega (who is highly knowledgeable about various heat decarbonisation options).

And finally, have you enjoyed your time at Imperial College? What do you plan to do next?

Map of Magallanes and Chilean Antarctica Region (Source: Wikimedia Commons)

I am hoping to publish a paper with Francisca and Paul, and I will continue working on this during the coming months. I might be speaking in a congress and will present my work to the Ministry of Energy in Chile.

It has been great working at Imperial College because it such a world-class international university and I really like the interdisciplinary environment. There are so many people doing relevant research here!

Dr. Francisca Jalil, a Research Associate at the Sustainable Gas Institute shares some insights from this year’s Sustainable Gas Research and Innovation 2018 conference.

In late September 2018, I attended the Sustainable Gas Research and Innovation (SGRI) conference, at the University of São Paulo, in Brazil. Our Institute hosts this conference every year with the Research Centre for Gas Innovation with the theme being around reducing the environmental impact of natural gas and also addressing topics such as Carbon Capture & Storage (CCS), and other carbon sequestration, storage, or usage technologies. The conference was especially interesting for me because of the range of topics from very detailed and local technological solutions (or process designs) to global energy systems models, in which the whole world’s energy sector and economic activities are modeled in long-term horizons.

One of the main things that caught my attention at this conference were the number of topics around the decarbonisation of transport. Reducing emissions and the carbon intensity of transport is an urgent matter for meeting the 1.5-2oC targets. It is also the topic of our Institutes next White Paper.

According to a recent report by the Mobile Lives Forum, after the energy sector, the transport sector is the second largest emitter of greenhouse gas (GHG) emissions. However, while world energy use in the power sector is decreasing, transport emissions continue to grow and might become the largest emitter by 2050. But it is also a very complex sector to decarbonise because of the lack of alternative low carbon technologies, especially for aviation, shipping, and heavy-duty road transport. These sectors are also very under-regulated when compared to light duty vehicles, for example being subject to very low or no fuel taxation. In addition to these complexities, transport is also a challenging sector to model compared to other economic sectors, as it has mobile demands. This is especially true for passenger and individual transport, as re-fuelling locations and times are always varying. This presents an additional challenge for modelling transport compared to -for example- heat demand in buildings, where locations are fixed and loads are predictable along days and seasons.

At the conference, I listened to several presentations on decarbonising transport, particularly road freight and shipping. According to the aforementioned report by the Mobile Lives Forum, out of the 14 countries studied Brazil had the second highest share of carbon emissions associated to transport in relation to the total carbon emissions of each country. This is, the transport sector in Brazil accounts for 44.8% of the country’s total carbon emissions, just closely after New Zealand with 44.9%.

The first talk that caught my attention was about how current road freight transport is so heavily reliant on diesel. The investigators used life cycle assessment to contrast this current scenario with natural gas and other diesel alternatives as potential substitutes. The study concluded that natural gas as an alternative fuel produces a quarter of diesel’s carbon emissions and almost no air pollutants at combustion point and that natural gas outperforms diesel in all environmental indicators studied.

Another talk highlighted research that compared liquefied natural gas (LNG) as a shipping fuel, with heavy fuel oil (HFO), marine diesel oil (MDO) and methanol from natural gas. The researchers concluded that as long as methane emissions produced in the engine and supply chain of LNG are controlled and kept under a certain limit, LNG as a shipping fuel can produce lower climate impacts compared to liquid fuels across all timescales. However, they emphasise the need to avoid supply chains with high embodied emissions of methane (this is, methane emitted throughout the processes associated with the whole extraction/production, transport, delivery, and use of fuels).

The third talk was about the use of natural gas in heavy goods shipping. The study emphasised that when looking at natural gas in shipping for diminishing GHG emissions and air pollution, it is very important to analyse the different engine types- which produce varying emissions or benefits across the range- together with the supply chain, to avoid embodied emissions. The researchers also proposed future policy options to regulate or incentivise certain production routes, in order to take advantage of cleaner methods.

Overall, the take-home messages for me were:

1) It is imperative to reduce emissions associated to heavy duty transport to stay on the path of our emission reduction goals.

2) When comparing fuel decarbonisation alternatives, it is very important to analyse not only different engine and fuel types, but also to take into account the different fuel production routes and life cycle emissions as these can have big impact.

3) As highlighted and recommended by one of these researchers and by the IEA, policies on transport “must raise the costs of owning and operating the modes with highest GHG emissions intensity to stimulate investments and purchases of energy-efficient and low-carbon technologies and modes”. This is, policies in transport need to be oriented towards making it expensive to use high-emitting transport modes, and cheaper to switch to cleaner transportation modes.

—

About Sustainable Gas Research & Innovation conference

The Sustainable Gas Research & Innovation 2018 conference brings stakeholders together to meet; share knowledge, exchange ideas, gain insight, and showcase expertise to fully understand the role of natural gas in the global energy landscape. This year’s event was included in the schedule of the Brazil-United Kingdom Year of Science and Innovation.

About Francisca

Francisca joined the Sustainable Gas Institute in May 2018, after completing her PhD in Chemical Engineering at Imperial College London. Francisca also holds an MSc in Sustainable Energy Futures from Imperial, and a Mechanical Engineering degree and MSc in Mechanical Engineering from Universidad de Chile.

By the time you finish your masters, you’ll know your thesis inside out. We challenged one of our researchers at the Sustainable Gas Institute to explain their research in a short one minute video as part of the ‘Research in a Nutshell Series’.

Sandro Luh is a visiting Masters student from the ETH Zurich. He is using the MUSE energy systems model to examine the potential of different strategies for reducing CO2 emissions in the industrial sector. This includes measures such as fuel switching, electrification and Carbon Capture & Storage.

The industrial sector is a key sector to decarbonise as it accounts for 24% of the total global CO2 emissions (2014).

We caught up with Jonathan before the talk to ask him about his research work.

Here’s the short Q&A interview on YouTube.

We asked Jonathan two questions:

As an expert in the world of gas markets, what do you think the role of the gas will be in the future? Can gas help us to decarbonise?

“Gas can help us decarbonise in the future but its not really easy to generalise across a lot of different countries and regions. In some countries gas will have a big role and in other countries it will not. It depends on how far you look ahead particularly the next 10 to 20 years.”

Could you describe very briefly what you mean by the key challenges for gas (unburnable and unaffordable) that you mention in your talk?

“By unburnable, I mean the challenge of phasing out the carbon element of gas in countries where targets are very important which is European and Some US states, and also in Japan and Australia.

But in the rest of the world, the more major challenge to gas is that people will not be able to afford it. In other words, it will be too expensive in relation to either the absolute level of income or because other fuels like coal or renewables will be cheaper. This is what we see in much of the developing world.”

If you would like to download the report, please visit the OIES website.

B.) A summary blog post: “A future of gas”

Sandro Luh, a research student at the Institute, has also written a short blog post for Energy Futures Lab.

The blog post summarises Jonathan’s talk and provides some of the key take-home messages.

Clarifying methane climate metrics, estimating uncertainties and exploring the sustainability of LNG as a shipping fuel.

Imperial College London and Enagás (the Spanish natural gas transmission company and Technical Manager of the Spanish gas systemthe Spanish energy company operating the national gas grid) are working together to shed some light on methane emissions from natural gas systems.

Researchers at the Sustainable Gas Institute (SGI) at Imperial have embarked on an intensive 9-month project to independently review the contribution methane emissions on climate change and to investigate the sustainability of LNG as a shipping fuel.

Dr Paul Balcombe, based in the Department of Chemical Engineering, explains the motivations behind the study:

“We know that emissions from shipping vessels have a significant impact on global climate change. Liquefied natural gas (LNG) fuelled shipping could potentially reduce the carbon footprint of the maritime industry relative to other marine fuels. But LNG’s sustainability credits as a marine fuel still need to be explored as natural gas is still a fossil fuel. We need the whole picture, and our focus will be on examining methane emissions.”

Combining knowledge and tools

The research is follow-on work from the SGI’s first White Paper which assessed the current knowledge of methane and CO2 emissions globally coming from the whole natural gas supply chain (i.e. extraction, processing, transmission, storage, liquefaction etc.) and detailed what factors affect emission these ranges (e.g. equipment, procedures).

The study will be carried out in three stages.

“One of the most important research requirements that we identified from our previous paper, was to fully explore what methane’s role is in climate change. Global Warming Potential (GWP) istypically the most common metric used for quantifying how much heat a greenhouse gas traps in the atmosphere. However, depending on the situation being addressed, it may not always be the most appropriate metric. The choice of climate metric can greatly impact on the perceived merits of different technology or policy approaches. We carried out a large review of available metrics and investigated both their suitability to specific situations, and the impact of using different metrics on final emission results,” says Dr Balcombe.

The second aim of the project stems from follow-on work from the White Paper (Methane & CO2 emissions from the natural gas supply chain). The new study will also investigate ‘hotspots’ of uncertainty surrounding estimates of methane emissions across different supply chain equipment and different methods of estimation. This will help industry identify ways to improve measurement and quantification of emissions.

The third part of the study will involve looking at what the role of LNG is as a shipping transport fuel, by considering shipping emissions but also across the whole supply chain from extraction, processing, transmission, storage, liquefaction, delivery and consumption. The work will look at greenhouse gases but also the air quality and economic costs compared against alternative fuel sources, including fuel oil and biofuels.

Claudio Rodriguez, Infrastructures General Manager at Enagás explains:

“As a leading company in the main sustainability indexes, Enagás is strongly committed with climate change and especially with methane emissions reduction all over the value chain. In this sense, partnership with SGI will help us to quantify how natural gas can contribute to a low carbon economy. This study will provide a framework for realistic and updated methane impact consideration, taking into account the different existing climate metrics as well as the uncertainty of both metrics and estimated emissions. Also, the study will provide a better understanding of methane fugitive emissions reduction existing potential at natural gas infrastructures and will help LNG to find its place in the maritime sector in the near future.”

The set of reports will provide a crucial reference document on emissions for academia, the gas industry and policy makers.

Dr. Pedro Gerber Machado works as a Researcher at Imperial Colleges’s Sustainable Gas Institute. Pedro is from Brazil and is interested in the sustainable development of energy production, thorough the development of new technologies and the application of policies. In this blog, Pedro talks about the inaction towards renewable energy in the last 30 years and how we need to change the history in order to have a true energy transition.

Dr. Pedro Gerber Machado works as a Researcher at Imperial Colleges’s Sustainable Gas Institute. Pedro is from Brazil and is interested in the sustainable development of energy production, thorough the development of new technologies and the application of policies. In this blog, Pedro talks about the inaction towards renewable energy in the last 30 years and how we need to change the history in order to have a true energy transition.